Inflation is the rate at which the prices of goods and services rise over a given period of time. In Nigeria, we see it in the way major goods like fuel, food, and transport costs swing violently.

If you want an in-depth explanation of why Nigeria experiences high inflation rates, read our previous post on inflation in Nigeria. Nigeria’s inflation rate is on the higher side. It is caused by big factors like crude oil dependence, more imports versus exports, government policies, and naira devaluation.

We are going to look at how inflation affects our personal lives and finances, and how to protect ourselves from it.

Inflation vs Your Spending

This is the frontline— where you immediately feel the effects of inflation. It reduces the buying power of your money. What your ₦10k could buy five years ago is not what it can buy now. The clearest evidence of this is that some of our smallest currencies have lost all or some of their value: the kobo, ₦10, ₦20, ₦50, and ₦100.

One of the easiest ways to see this in your own spending is to track your expenses from month to month and year to year. You might realize that your monthly spending has subtly risen over time, and that things that used to cost less now cost more.

Self-Defense.

You can’t stop inflation as an individual, but you can change how exposed your spending is to it.

- Track your spending: Inflation is gradual and not always very obvious. Tracking makes you aware of price increases over time. It shows you which categories are inflating fastest.

- Budgeting: This is about planning and prioritizing what you spend on. It doesn’t stop prices from rising nor magically make your income sufficient, but it does force you to be very specific about what to buy first and what to cut out. It protects your essential expenses from being overtaken by non-essentials. Budgeting always beats freestyle spending any day, any time. Let essentials like rent, transport, and food take first claim on your money, while non-essentials should take the volatility.

- Find cheaper alternatives and discounts to expensive items exposed to inflation when you can.

- Buy in bulk, but cautiously, the items you already consume regularly, e.g., buying a bag of rice versus buying measured rice every month, or buying a carton of chicken versus buying in kilograms every month. Buying in bulk can reduce your exposure to inflation, but only when it doesn’t strain your pocket.

- Buying earlier. Some expenses benefit from buying them earlier. For instance, a washing machine bought today delivers value for years after and protects you from price increases, versus if you had hired a dry cleaner or washerman whose service charge will increase as inflation rises. Buying early works if you already need the item, it has a long, useful life, and the item’s function doesn’t change rapidly.

Inflation vs Your Salary: The Quiet Pay Cut

Salary earners are the most affected by rising costs because their pay is usually fixed. Business owners, for instance, are able to adapt to rising prices because they can simply pass the costs to customers by raising the prices of their goods and services.

To better understand how salary earners are affected, let’s look at how inflation affects a hypothetical salary earner called Tola. Assume Tola started earning ₦300,000 when she started working at ABC Company back in December 2024; now it’s December 2025.

₦300K is her nominal salary (i.e the documented salary on paper), while her real salary means the actual purchasing power of her salary, not the paper figure.

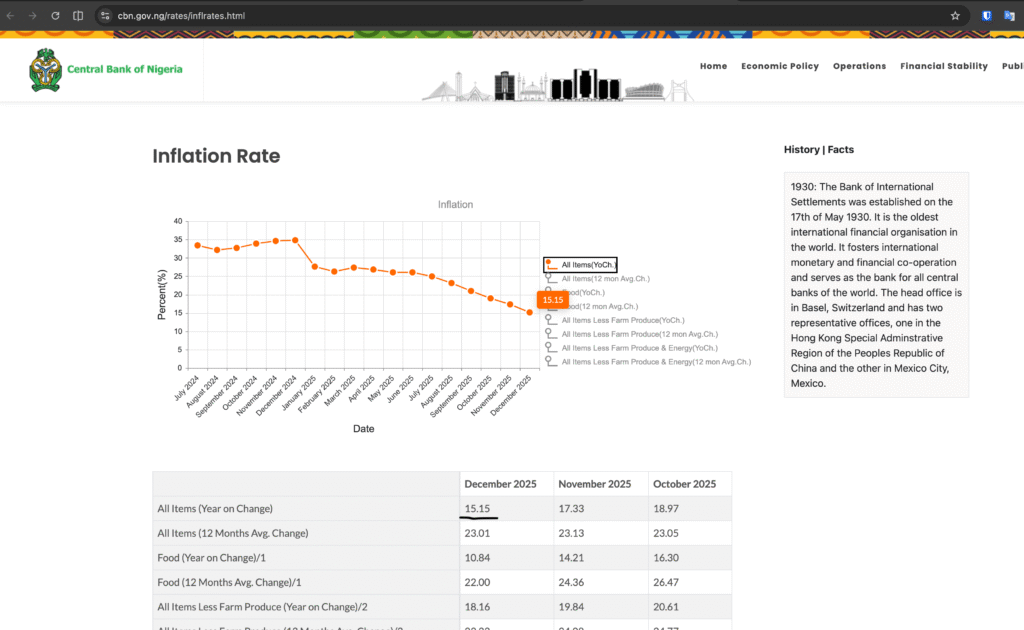

To check the current inflation rate, visit cbn.gov.ng/rates/inflrate.html. The one you want if you want to know the inflation rate in one year is All items(YoCh).

For instance, as at December 2025, the inflation rate for All items (year on change) is 15.15%. That means, in the one-year period from December 2024 to December 2025, prices have increased by 15.15%. If something costs ₦100 in December 2024, it now costs: (100 x 0.1515) + 100 = ₦115.15.

Calculations

To calculate Tola’s real salary value in December 2025 using the inflation rate:

Nominal Salary: ₦300,000

Inflation rate: 15.15%

15.15% = 15.15/100 = 0.1515

Real salary Formula = Nominal / (1 + inflation rate)

Real salary = ₦300,000/(1 + 0.1515) = ₦260,530

So, although Tola is paid ₦300k, her salary buys what ₦260,530k used to buy a year earlier.

Nominal salary yearly: ₦300k x 12 = ₦3.6 million.

Real salary yearly: ₦260,530 x 12 = ₦3,126,360.

Difference: 3,600,000 - 3,126,360 = ₦473,640

Without the raise, Tola effectively lost 473k in one year. This is why annual raises deceive people. If Tola gets a 10% raise on paper, her ₦300k becomes ₦330,000. The so-called raise is still just around ₦286,583 in 2024 purchasing power.

Tola would need to get a 15.15% raise (₦345,450) to match what her salary could buy back in December 2024.

15.15% raise = (0.1515 x 300,000) + 300000 = ₦345,450

Real figure = 345,450/(1+0.1515) = ₦300,000

Many people think… “Yay, I got a raise,” but they haven’t really gained any extra ability to buy more things. They’ve just kept pace with inflation, sometimes, barely. When you get an actual raise, if it doesn’t at least match inflation rates, then you overestimate how better off you are.

Self-Defense

- Improve your employability skills so that your skills are in demand enough for a better-paying job.

- Once you notice that your salary has stagnated and inflation has eaten into it, and even your raises don’t catch up with inflation, it is time to either negotiate for a raise that matches/beats inflation or switch jobs with higher pay.

- Improve your negotiation skills by asking for what you’re worth and what matches the current economic reality.

- Diversify your income; try a side hustle or a business, freelance work, content creation, writing, teaching, etc

- If possible, earn in stronger currencies like the dollar or pound. This offsets a lot of the exposure to high inflation that Nigeria has.

- Avoid high fixed expenses, especially long-term ones like very high rent, because they can get even more expensive during inflation.

The takeaway is that your salary is not a one-time installment; it’s a contract that can be negotiated. Pay close attention to the difference between your nominal on-paper salary and the real value of your salary. Learn how to calculate the figures for yourself.

Inflation vs Your Savings

Saving money is a very great habit to have, but to fully benefit from saving money, you have to make sure that your money maintains its purchasing value.

It’s not enough for your money to be saved; it must be protected.

Physical Cash

One of the biggest mistakes a person can make is to save money in physical cash. Aside from the obvious risks like currency damage and theft, as prices increase yearly, the value of the physical cash goes down. It never generates any interest.

Bank Savings

While bank savings are better than keeping physical cash at home, it’s still not enough to protect your money from Nigeria’s inflation in the long run. In some foreign countries, high-yield savings bank accounts (3-5% interest) might be able to keep up with inflation rates (2-3%) and preserve money value, but in high inflation economies (> 14%) like Nigeria, that assumption breaks down completely. In Nigeria, long-term savings in banks guarantee the loss of purchasing power.

Emergency Funds

When it comes to saving money in a bank account, an exception can be made for emergency funds because the whole point of emergencies is to be able to access it immediately when you’re in need. So obviously, emergency funds should not be tied up in investment instruments that are hard to sell. At the same time, it should not be left to completely lose its value either. A balance can be had.

Assume ₦1m as your emergency fund, 10% of it could be kept in a bank (₦100k) for easy withdrawal during an emergency, while the rest (₦900k), could be kept in an easier-to-sell instrument like an MMF.

MMFs can be sold in 24 hours. They track short-term interest rates, which are set by the CBN. When inflation rates are low, interest rates go down, and vice versa. This makes MMF good enough to preserve purchasing power, but not necessarily good for growing your money, making them a practical solution for emergency savings in a high-inflation environment.

Self-Defense

Savings do not automatically mean your money is safe, as we’ve learned. If your savings generate interest at a rate less than the inflation rate, it means your money is shrinking in real terms.

- Avoid idle cash, especially in physical form, except for short-term transactions.

- Understand that banks are great for salary inflows, bills, emergency cash access, short-term holding, but bad for long-term savings and wealth preservation.

- Use your MMFs as a temporary savings buffer. They are better than banks because they track short-term interest rates. Interest rates tend to rise when inflation rises. The MMFs won’t make you rich, but they slow down the damage of inflation.

- Separate your emergency funds from the rest of your long-term savings and investments. Emergency funds are designed to be instantly accessible.

- For the rest of your savings, you will need to look into more growth-focused investments that surpass inflation.

- Reduce currency risk. Saving only in Naira exposes you to local inflation and devaluation, but diversifying into stronger currencies with lower inflation can reduce risk, e.g., USD, GBP, Euros.

Inflation vs Investing

Investing your money, just like saving, is a great habit to have, but the how matters. For investments to be profitable, they must generate returns higher than the inflation rate. For instance, if the inflation rate is 15% and an investment returns 12%, that is a negative return of -3%. If the returns are greater than 15%, then it’s a positive return.

Fixed income investments like bonds and treasury bills are the ones affected by Inflation the most, because their returns are fixed in advance. Let’s say you have bought a government bond at 12% interest that matures in 5 years. The bond’s interest rates will not change even when inflation rates bypass 12%. That’s what makes them vulnerable to inflation.

Types of Assets

Different asset types behave differently under inflation.

Inflation-losing Assets

They look safe, but they lose purchasing power because their returns are fixed. They don’t adjust to inflation rates. Example, saving accounts, fixed-rate bonds, fixed deposits.

Inflation-preserving Assets

They don’t make you richer, but they help you preserve your purchasing power. Examples, MMF, treasury bills, etc

Inflation-beating Assets

They grow because they are tied to the ebbs and flows of the real economy. Their income or value rises as prices rise. Example businesses or equities, rental real estate, and certain commodities.

An asset rising in nominal value does not mean it beats inflation. For instance, if a piece of land rises from ₦5 million to ₦20 million over 20 years, that looks like growth on the surface, but if prices rise even faster over the same period, the real value may not have increased at all.

Self-Defense

The key feature to check for when selecting investments that can outpace inflation is that they should, at best, beat inflation and, in the worst case, preserve the value of your assets.

Before buying an asset, ask the question:

- Does income or value for this asset adjust when prices rise?

- Is the return from this asset fixed or flexible?

- Is the asset tied to real economic activity?

Final Notes

Inflation isn’t just an abstract concept reported in the news. It is something that affects your cost of living in very visible and measurable ways: from what you can buy to how far your salary stretches to the value of your savings and investments.

The good news is that you can start taking stock of all the parts of your financial life that inflation can affect and take necessary steps to defend yourself.

- Spending: Track your expenses and budget your money.

- Income: Calculate the real value of your income and invest in your skills to increase earning potential.

- Savings: Avoid leaving cash idle and consider accessible instruments like MMFs to preserve value.

- Investing: invest wisely. Choose assets that have the potential to outpace inflation while keeping a balanced approach to risk.